Pi KYC rumor turns privacy into the real price

I break down Pi Network’s KYC rumor, why it’s unverified, and how to think about privacy, compliance, and user value.

A practical breakdown of Pi KYC rumors, privacy trade-offs, and a copyable compliance checklist.

I’ve been watching crypto communities do this dance for years: one post hints at regulatory acceptance, the room lights up, and suddenly everyone is acting like a rumor is a roadmap. Pi Network is having one of those moments right now. A community post on HOKANEWS.com picked up a claim from @pitown89 on X that Pi KYC might be recognized in the US and EU. That’s a huge statement if it were real. It also happens to be exactly the kind of statement that gets people to confuse “maybe” with “confirmed.”

What bothered me is not the speculation itself. Crypto communities speculate constantly. What bothered me is how fast identity, compliance, and value get mashed together like they’re the same thing. They’re not. KYC can be a real compliance tool, but it can also be a privacy tax. Regulatory alignment can help a project, but it does not magically make a token valuable. And a community saying “we’re recognized” is not the same as an actual regulator saying it. I’ve seen too many teams talk themselves into a narrative before the paperwork exists. That’s how people end up overcommitted, underinformed, and weirdly defensive when the facts don’t land the way they hoped.

So I’m going to unpack the claim the way I would for a teammate: what the article says, what it does not say, and how I’d think about KYC, trust, and user value if I were building around this stuff.

Source anchor: the trigger here was HOKANEWS’s article, “Pi Network KYC Recognition Claim in US and EU Sparks Privacy and Value”, which cites a community post from @pitown89. The article itself says the recognition claim is speculative and unconfirmed.

The rumor is not the regulation

Get the latest AI news in your inbox

Weekly picks of model releases, tools, and deep dives — no spam, unsubscribe anytime.

No spam. Unsubscribe at any time.

“Pi KYC may be recognized in the United States and European Union… However, there is no official regulatory confirmation publicly validating this claim.”

What this actually means is simple: somebody in the community said something big, and the article correctly labels it as unverified. That distinction matters more than people want to admit. In crypto, a lot of bad decisions start with a screenshot and end with “I thought it was official.”

I’ve run into this exact failure mode in product work. Someone hears “the platform supports enterprise compliance,” then assumes the feature is approved everywhere, for every use case, with no legal review needed. No. Support is not approval. Capability is not recognition. And community excitement is not a regulator.

If I were reading this as a user, I’d ask three questions immediately:

- Who made the claim, and where is the primary source?

- Did any regulator, exchange, or official body publish a confirmation?

- Is the article describing a verified status or just a discussion inside the community?

How to apply it: when you see a compliance claim, split it into three buckets: community speculation, project statement, and regulatory confirmation. Only the last one changes legal reality. Everything else is commentary.

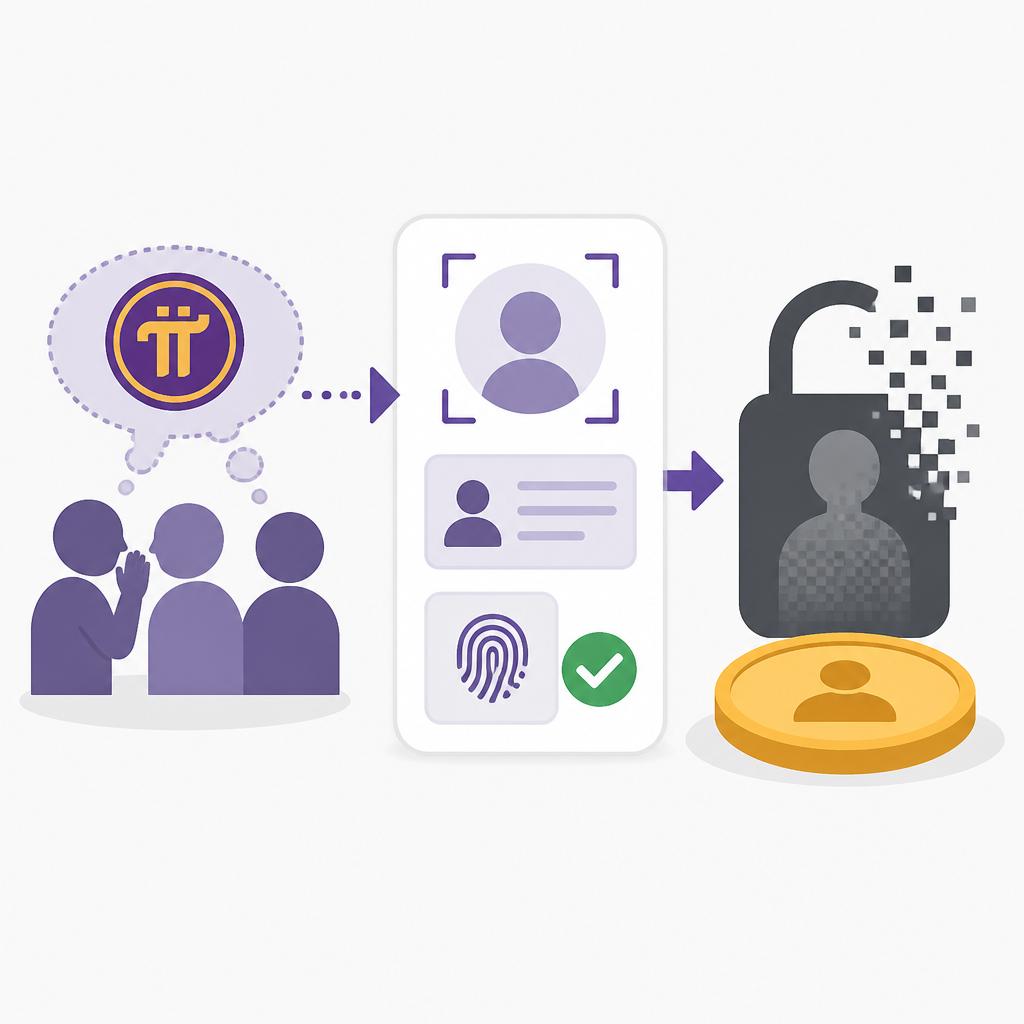

KYC is a trade, not a badge

“Users may be ‘trading something in return’ for participation in KYC enabled ecosystems.”

This line is the most honest part of the whole discussion. KYC is not free. You give up data, time, and a bit of control in exchange for access. That trade can be reasonable. It can also be badly explained, overbroad, or stored in ways users never expected.

People in Web3 like to talk as if decentralization automatically cancels out identity collection. It doesn’t. If a platform wants to operate in regulated markets, it often needs to know who you are. The real question is not “KYC or no KYC.” It’s “what data is collected, who stores it, how long it lives, and what happens if the platform gets hacked or changes policy?”

I’ve seen teams treat identity as a checkbox. That’s a mistake. Identity systems are infrastructure, and infrastructure has blast radius. Once you collect personal data, you own the operational burden that comes with it. Retention policies, access controls, breach response, user consent, vendor contracts, deletion requests. The whole annoying stack.

How to apply it: before you join any KYC-gated ecosystem, read the privacy policy like it’s a contract, because it is. Look for data categories, retention periods, sharing terms, and deletion rights. If those are vague, assume the risk is on you.

Compliance can help adoption, but it does not create value by itself

“Regulatory alignment can enable broader exchange access, institutional participation, and user confidence.”

This is where a lot of crypto narratives get lazy. Yes, compliance can open doors. Yes, regulated access can matter. But value is still value. If a token, network, or app has weak utility, a compliance story won’t fix that. It just makes the weak utility easier to list in more places.

The HOKANEWS piece frames regulatory alignment as a path to mainstream adoption, and that part is directionally right. If a project wants serious exchange access or institutional participation, it needs to behave like a grown-up. That means formal processes, not vibes. It means audits, licensing, and jurisdiction-specific rules. Not “the community believes.”

But I’ve also watched projects over-index on legitimacy theater. They chase the appearance of being ready for the big leagues before they’ve built anything people actually need. Then the token price becomes a substitute for product-market fit. That’s backwards.

How to apply it: when you hear “regulatory alignment,” ask what it unlocks in practice. Better on-ramps? Better custody? Better access to fiat rails? If the answer is vague, the compliance story may be doing more marketing than engineering.

- Compliance can reduce friction with exchanges.

- Compliance can help with legal risk management.

- Compliance does not guarantee demand, usage, or token value.

Privacy is the part communities underprice

“In blockchain ecosystems that incorporate KYC, users are required to submit personal information to verify identity.”

This is the trade-off people keep pretending is abstract until it hits their inbox. Privacy is not just about “I don’t want strangers to know my name.” It’s about what a platform can infer, retain, and reuse from the data you hand over.

The article points out that users may not fully consider the implications of participating in identity-verified ecosystems. I agree, and I think the problem is worse than that. Most users don’t have the context to judge whether a KYC flow is narrow and well-guarded or broad and sloppy. They just see “verification required” and keep moving because they want access.

I’ve had to audit product flows where the team claimed they only needed a document scan, but the vendor pipeline quietly stored more than the team realized. That’s the kind of mess that turns a “simple compliance feature” into a liability. Data minimization is not a slogan. It’s what keeps a small feature from becoming a future incident report.

How to apply it: if you’re designing or evaluating a KYC process, ask for data minimization by default. Collect only what you need. Separate identity storage from product analytics. Give users a clear deletion path. And if you can’t explain the data lifecycle in one minute, you probably don’t understand it well enough yet.

Community hype is not a substitute for official language

“The statement should be understood as community speculation rather than verified regulatory status.”

This sentence is doing a lot of work, and it should. In a healthy ecosystem, that’s the sentence people remember. In an unhealthy one, it gets buried under reposts, price talk, and people building elaborate theories from one vague post.

What I take from this is that the article is useful precisely because it refuses to overstate the claim. It says the rumor exists, it explains why the rumor matters, and it stops short of pretending there’s formal approval. That’s the right editorial move. I wish more crypto coverage did that instead of laundering speculation into certainty.

There’s also a social lesson here. Communities love certainty because certainty feels like conviction. But in practice, certainty without a source is just emotional leverage. It pushes people to act before they’ve checked the actual status.

How to apply it: when you see a claim about regulation, look for the exact wording. Is it “recognized,” “compatible,” “aligned,” “under discussion,” or “approved”? Those are not interchangeable. If the source can’t be precise, neither should you.

What I’d do before trusting any KYC-heavy network

If I were deciding whether to participate in a KYC-heavy crypto ecosystem, I’d treat it like a risk review, not a fandom choice. The project can be promising and still deserve skepticism. Those are not opposites.

Here’s the checklist I’d use before I put my identity behind it:

- Find the primary source, not just a repost.

- Check whether any regulator or official body has spoken.

- Read the privacy policy and retention terms.

- Look for a clear deletion or account closure process.

- Separate token speculation from actual utility.

- Assume community enthusiasm is biased until proven otherwise.

I’d also compare the project’s claims against basic compliance references from actual institutions. For general KYC and AML context, I’d start with the U.S. Financial Crimes Enforcement Network and the European Banking Authority. For privacy expectations in the EU, the GDPR overview is a useful baseline. And if I want to understand how a project presents itself publicly, I’d go straight to the project’s own site, not just the community echo chamber.

How to apply it: don’t ask, “Do I believe this project?” Ask, “What data am I giving up, what do I get back, and who can verify the claims?” That framing is a lot less romantic, but it saves you from bad assumptions.

The template you can copy

## KYC claim review template for crypto projects

### 1) What was claimed

- Claim:

- Who said it:

- Where it appeared:

- Date:

### 2) What is actually confirmed

- Official source URL:

- Regulator / exchange / project statement:

- Exact wording:

- Status: confirmed / unconfirmed / speculative

### 3) Privacy review

- Data collected:

- Why it is collected:

- Where it is stored:

- Who can access it:

- Retention period:

- Deletion path:

- Cross-border transfer risk:

### 4) Compliance review

- Jurisdictions involved:

- KYC/AML requirement:

- Licensing or audit evidence:

- Any public regulatory filing:

- Any legal disclaimer:

### 5) Value review

- What user benefit exists today:

- What utility is promised later:

- What is measurable now:

- What depends on speculation:

### 6) Decision rule

- If the claim is unverified, do not treat it as official.

- If privacy terms are unclear, assume the user bears the risk.

- If utility is weak, do not confuse compliance with value.

- If the source is only community chatter, wait for primary confirmation.

### 7) Short verdict

- My read:

- My risk level:

- My next action:

That’s the whole game for me. Separate rumor from regulation. Separate compliance from value. Separate user enthusiasm from user protection. Once you do that, a story like this gets a lot easier to read, and a lot harder to be fooled by.

Original source: HOKANEWS.com. I used that article as the base and added my own breakdown, examples, and decision template.

// Related Articles

- [IND]

Vector databases will reshape financial search, not replace core syst…

- [IND]

Milvus 3.0 adds lake-native vector search

- [IND]

Google’s Q2 2026 results prove AI spend is now the story

- [IND]

AI regulation in India is now a business risk

- [IND]

Europe should standardise the AI Act through harmonised technical rul…

- [IND]

AMD and Anthropic’s 2GW deal reshapes AI supply